Alessandra Nibbio is the InFiNe.lu sholar to attend the 2017 Boulder Microfinance training. She gives her insights of her 3-week experience in Turin:

Week 1:

Week 2:

Week 3:

The last week of 23rd Annual Boulder Microfinance Training (MFT) Programme has come here in Turin, but there are still vivid discussions among the faculty and the training participants which deserve to be mentioned and explored.

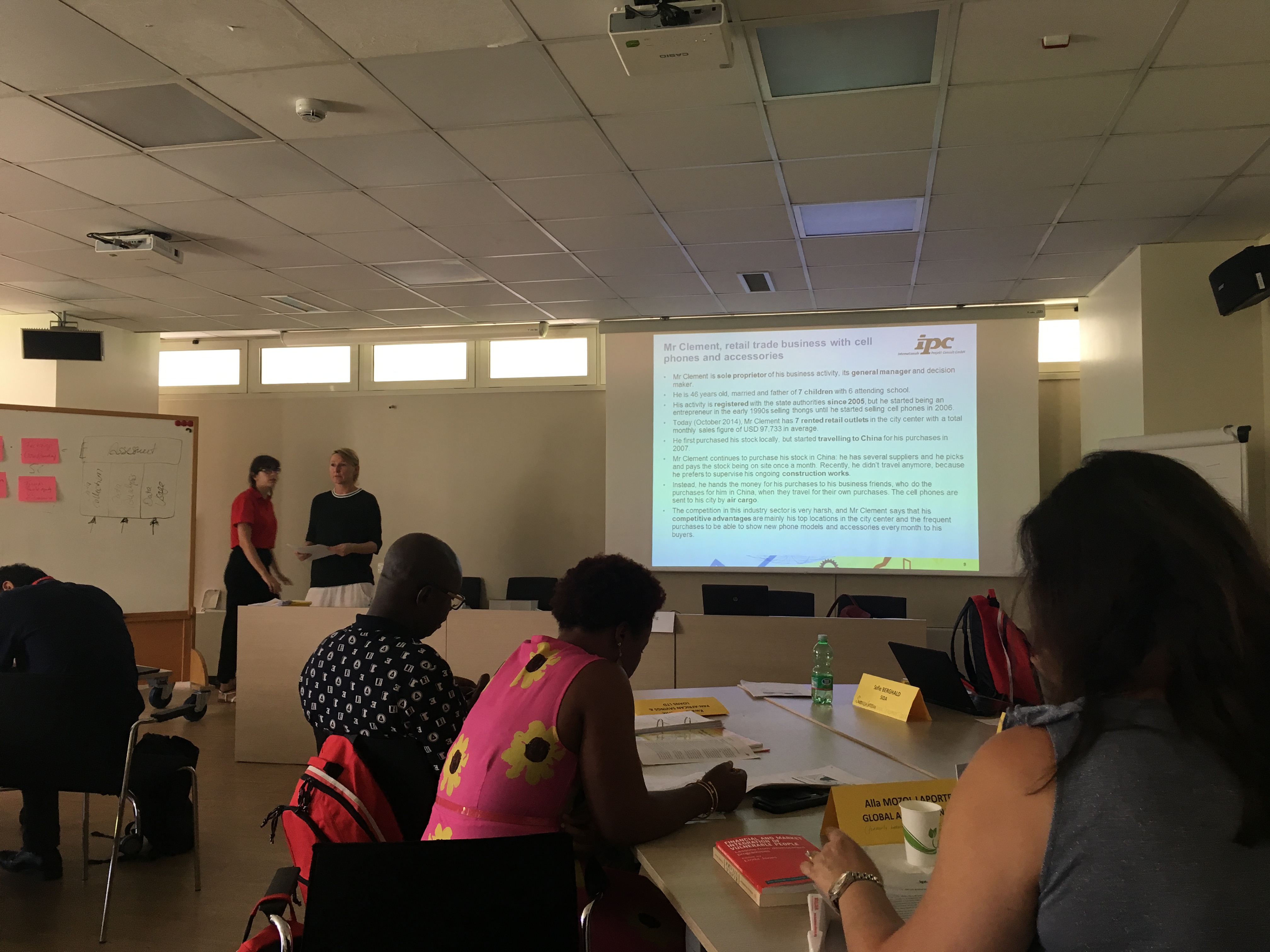

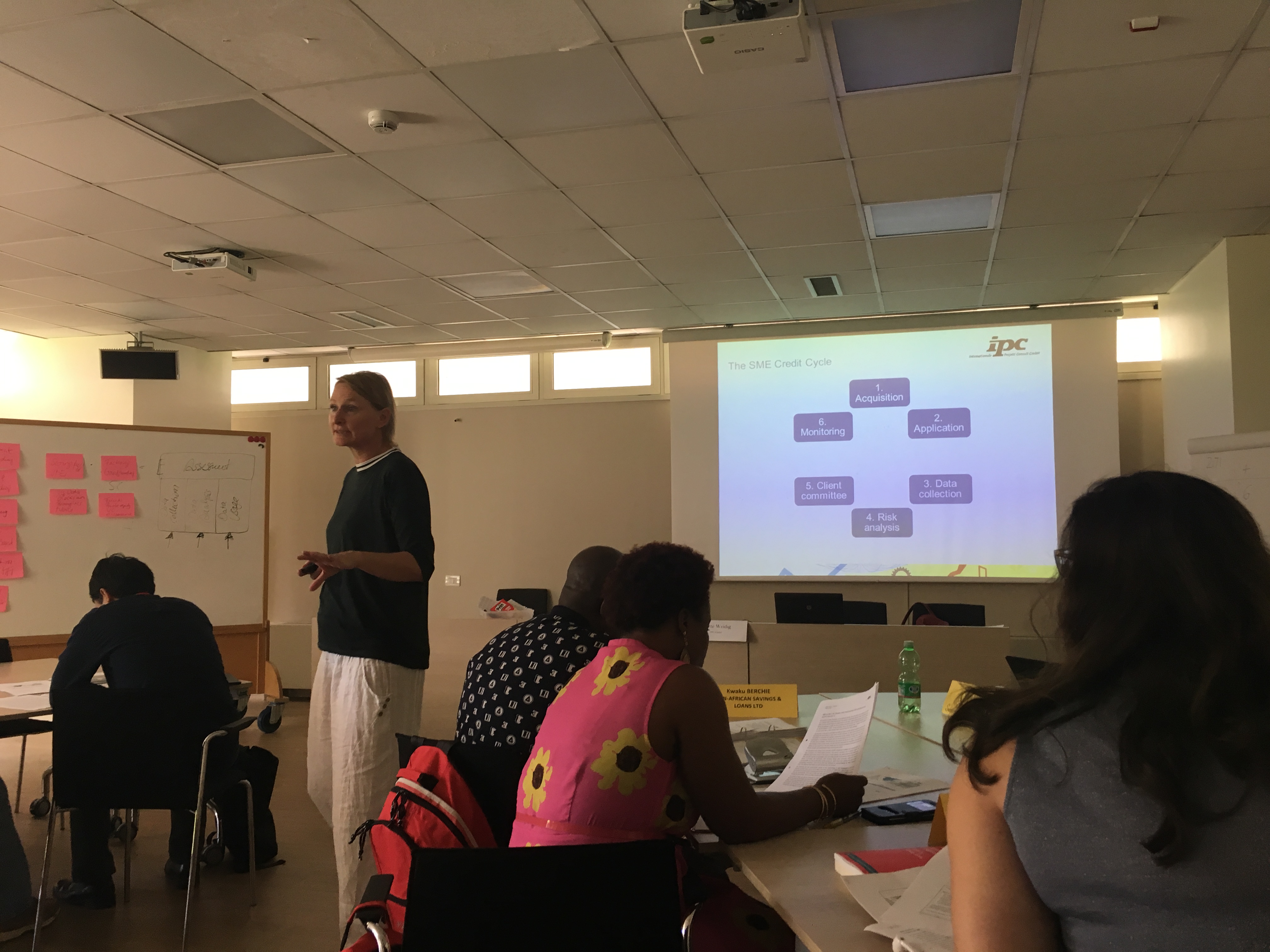

With this regard, one of the two courses I chose for this last week has been “SME Finance”, to integrate and complete my learning experience with some knowledge about Small and Medium Enterprises (SME) financing, which currently represents a crucial portion of the microcredit beneficiaries.

The professor, Ms Dörte Weidig, is Managing Director of IPC GmbH, responsible for acquiring new and managing existing consulting projects with financial institutions in Africa and Latin America, as well as for developing and co-ordinating skills development and education finance initiatives worldwide. She is a highly qualified banking expert with solid senior management experience and in-depth knowledge of MSME finance, with proven track record in strategy design and implementation.

The five days module aims to give an overview of the methodology of SME loans, presenting proven analysis techniques and the structure of the financing needs of SMEs.

The complexity of this topic already shows up looking at the definition of “Small and Medium Enterprises”, which can vary greatly from country to country and between authorities, institutions and financial regulators who use it.

Although, in theory, the main factors determining whether an enterprise is an SME should be:

Ms Weidig explained that nowadays SMEs are at the centre of attention because in many countries these businesses are the backbone of the economy and they employ large numbers of people.

Indeed, based on IFC data, SMEs count for 90% of all businesses worldwide and they make up for over 50% of employment in the world, being the largest employers in many low-income countries.

Furthermore, it has been demonstrated that there is a positive correlation between SMEs and capital investments.

The professor used the example of two countries: Germany and Kenya.

Considering Germany, which is a country doing well compared with many others, it results that 99% of the firms belong to SMEs and approximately 95% are family owned, being a leading generators of jobs.

While, in Kenya, even if there is a valuable contribution of this industry to the country GDP (ca. 50%), there are several constraints which are inhibiting SMEs growth such as, corruption and difficulties in accessing funds.

Generally speaking, the impressive growth in SMEs portfolio around the world has been mainly driven by the involvement of domestic banks but, there are still several obstacles for SMEs especially looking at developing countries.

Indeed, it results that 75% of SMEs have some kind of banking relationship but, just 30% of them have access to credit.

In addition, most of the SMEs do not have any records available which result in a lack of business documents and structured information, making them an “undesired” and “uncertain” client for financial institutions.

This shaky situation is getting more critical considering the fact that, on the other side, financial institutions do not have most of the time neither qualified staff able to understand businesses and to conduct adequate credit risk assessment, nor products and services needed by SMEs.

Therefore, it appears clear that currently a financing gap exists, although SMEs are not totally excluded from financial sector, as serving heterogeneous SMEs is more difficult than serving corporate and micro clients.

With regard to financial institutions, there are just few tailoring products, processes, tools and people to SMEs, as they are rather too risk adverse to work with informal or semi-informal SMEs.

But then, how to find the appropriate trade-off between financial sustainability and access to finance for SMEs?

Financial Institutions and SMEs will have to explore together how to strengthen their relationship and spread around good practices to be replicated.

In general, what should be done in practice by these two actors:

Therefore, the next step is on financial institutions, which can make better efforts to excel in SMEs finance as – to date – they have some unique selling points in serving SMEs.

Despite there is still a big portion of unserved SMEs in emerging economies, as mentioned, it appears that Development Financial Institutions, Donors and Investors in general are looking more and more at this topic less “purely” than before.

Indeed, the interest of investors for this segment is becoming broader and integrated with more comprehensive market perspectives such as the increase of employment or the provision of sustainable energy solutions.

In this sense, SMEs should get the ball on time and try to predict which are the trends to make their businesses more appealing to MFIs as well as Investors in order to survive and eventually grow aligned with the market.

For this last article, which represents the completion of my journey at Boulder, I would like to report one of the most interesting discussion which took place during this third week of training.

On Wednesday 2nd, a special session has been held during the lunch break on Islamic Microfinance, led by Ms Bursha Shafiq, representative of the State Bank of Pakistan.

Ms Shafiq speech started with an overview on the recognised growth of inclusive development occurred during the last decades.

In this context, microfinance has emerged and gained popularity as one of the most effective tools to reduce poverty, and bring to financial inclusion.

However, despite many research studies reporting the positive economic and social impact of microfinance programmes, there is also a significant portion of literature showing that microfinance does not have brought sustainability in improving its client’s life.

Indeed, it has been proven that it is not only the financing gap, but the lack of social intermediation which is a major hurdle towards improving the social status of those below the poverty line.

When she referred to “Social intermediation”, she meant the process in which investments are made in the development of both human resources and institutional capital with the aim of increasing self-reliance of marginalised groups, preparing them for formal financial intermediation.

In this sense, Islamic microfinance can play a more effective role in poverty reduction compared to traditional microfinances.

This role is mainly due to the nature of Islamic financing contracts, which make sure that the poor gets the intended productive real goods and services, and their potential effective use becomes instrumental in bringing the poor out of the poverty trap.

Also, the ultimate goals of Islamic finance is to help the poor, ensure equitable distribution of wealth and enhance social welfare, while the commercial aspect dictates generation of profit through targeting the underserved segment, making them contributors to economic growth and development.

This obligates Islamic microfinance institutions to consider the poorest as target clients, and also to monitor and supervise the use of financing, while minimising the operational inefficiencies of conventional microfinance.

This advantage of Islamic microfinance, of being more effective and sustainable, lies in its structure which is fundamentally different from the structure of conventional microfinance.

There are differences in products and strategies of both industries, through which financial access is extended to a financially deprived segment.

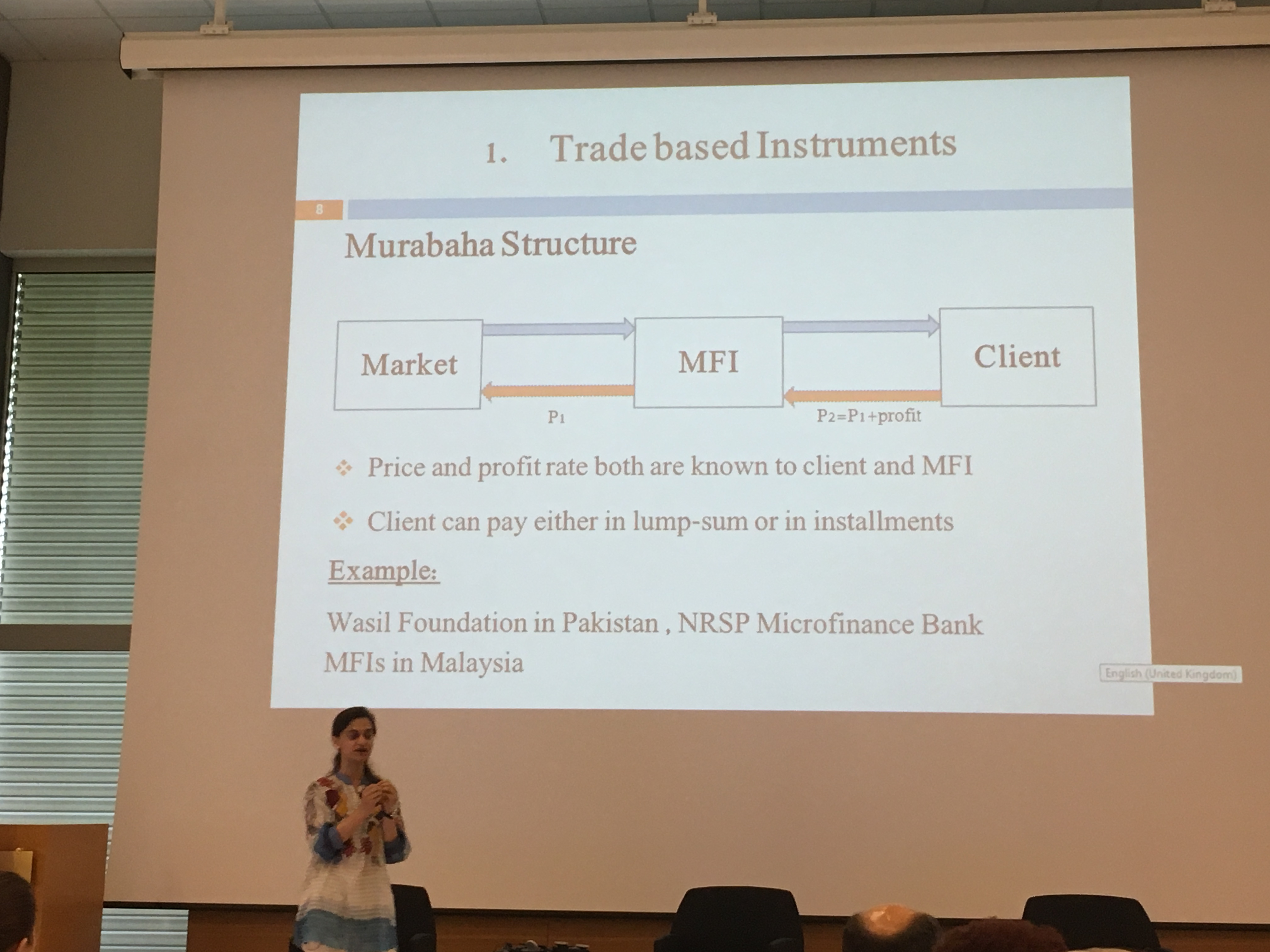

With this regard, there are two main approaches used in Islamic microfinance:

The target group of this category is the extremely poor, economically inactive, which need funds for their primary necessities.

However, it is crucial to make them economically active by providing some training or equipping them with technical skills making their social and economic uplift sustainable.

The instruments for this group may be classified in the following two categories:

However, sustainability becomes challenging and institutions are required to combine these charitable instruments with profit based instruments.

2. Qard hasan

Qard hasan, an interest free loan, is considered the purest form of Islamic financing to help the poor. The essence of this instrument is that the borrower only pays back the principal amount.

For MFIs, this instrument may be used for both saving and financing purposes. As it is zero return financing, it can be used to provide microfinance to the needy for either consumption or investment, and the borrower will only pay back the principle amount.

Along with being a zero return financing facility, this product has the flexibility of allowing extension in the repayment of loan amount.

All these instruments represent interesting and innovative ways of providing access to finance, however, their presence is still very low and it is concentrated only in few countries depicting a huge potential market for Islamic financial institutions as well as microfinance institutions to capture the faith sensitive microfinance clients.

If you are interested in learning more about this topic, please visit the Global Islamic Finance Report website.