Alessandra Nibbio, junior consultant at Innpact, is the InFiNe.lu scholar attending the 2017 Boulder Microfinance Training.

She is sharing her experience of the training. Find out what are the insights of her first and third week and the two articles concerning her second week:

The second week of the Boulder Microfinance Training has started in Turin and new causes for reflection are just around the corner.

The second week of the Boulder Microfinance Training has started in Turin and new causes for reflection are just around the corner.

Indeed, here at Boulder you meet every day new people currently working in the microfinance industry or who are approaching the industry.

The audience is mainly constituted by professionals with different background (MFIs, Donors, Investors, Regulators, Consultants, etc…), someday they take part to courses as students, sitting just next to you, and some other days they become active member of the faculty, with unpredictable exchanges of roles, which contribute to further animate the debate.

With this regard, on Monday morning, while sitting at the Master Class, I saw in front of me presenting on the stage, this charismatic young woman that until last Friday was attending the course on financial performance measurement with me.

Gayatri Murthy is Financial Sector Analyst on the Customers at CGAP, where she supports financial service providers (FSPs) in the adoption of the customer-centricity approach through research, resources and partnerships.

In partnerships with FSPs in India and Kenya, she works on building insights into the needs, behaviours and preferences of their low-income consumers to improve the delivery of financial products and services.

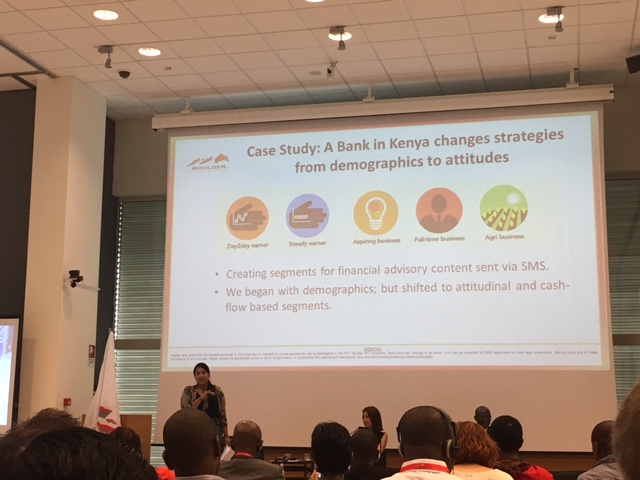

During her speech, she presented the importance and effectiveness of using segmentation for MFIs during their daily activities, from sizing the market to client’s retention.

Indeed, customer segmentation allows organisations to divide a market into subsets of customers that have, or are perceived to have, common needs, interests, and priorities; then design and implement strategies targeted towards them.

Nowadays, customer-centricity is a concept that is becoming extremely important as it can guarantee a significant advantage for institutions against their competitors and that practically everyone agrees with, but which is still not always implemented.

Indeed, to effectively put the needs and aspirations of customers at the centre of business strategies and decision-making, MFIs may have to rethink their operations and invest significant effort and resources to change not only business operations but also organisational mind-sets.

However, this “significant effort” is most of the time overestimated.

As a matter of fact, with regard to additional costs for the MFI, the organisation can produce great results with few resources, including focusing on information that’s already gathered in-house and readily available.

There are several ways to conduct a segmentation among customers and it is just a question of understanding which methodology applies for each particular situation.

Segmentation could be mainly divided in:

Although the segmentation methodologies have not changed much over time, the approach to data collection has changed.

Indeed, qualitative research now are mainly based on the relationship between the MFIs and customers which starts more rapidly and informally, having conversations with a group of customers while they visit the branch.

This represents a great way to learn about customers experience without getting into the logistics. Furthermore, “customer sketches” are becoming popular, as thanks to a simple exercise, the MFI starts characterising clients and learn about potential lack of information.

On the other side, new technologies have changed the quantitative side of the data collection, so MFIs need to have the right message and product available in the right channel when a potential customer comes looking.

All these aspects belong to the new frontier of segmentation, channel and product strategy.

Segmentation can help these organisations to serve low income markets by understanding important common characteristics of their customer base, which can make the difference between an underutilised service and one that resonates with customers.

Furthermore, conducting a satisfactory segmentation, and offering a range of tailored services, helps MFIs reducing risks by diversifying across products and accommodate customers’ needs.

Therefore, segmentation constitutes one crucial step in a complex journey, where the ultimate goal is to help build customer-centric FSPs, where all business operations are focused on the customer and continuously informed by insights on their lives and their needs and which begins with understanding how access to financial services can add value to the lives of lower-income customers.

During the second week of the Boulder Microfinance Training I chose two complementary courses, one focused on the interest rates set up, and the other on the main microcredit methodologies.

I registered to these two courses in order to have a better understanding of MFIs strategies and lending activity processes.

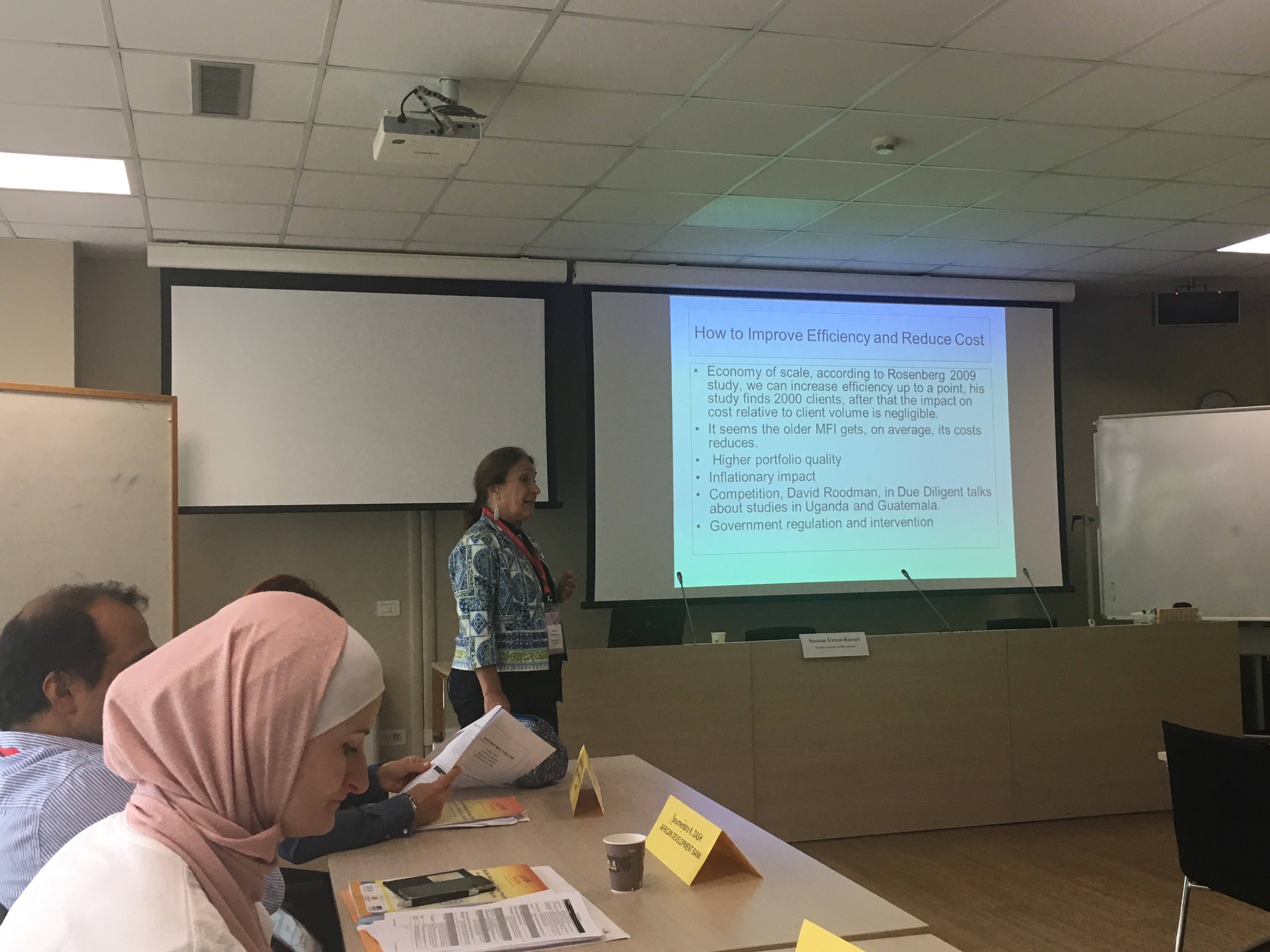

The professor, Ms Sousan Urroz-Korori, is a senior faculty in International Finance Development and an Executive Administrator at University of Colorado, Leeds School of Business at Boulder, with over 20 years of experience in private and public sectors.

This five day intensive module focused on understanding all aspects of risk associated with interest rates, both from an investor’s and the microfinance institution (MFIs) point of view, including the real cost of capitalisation.

The course has initially provided an introductory overview of financial risks which affect interest rates (liquidity risk, FX risk and macroeconomic risks) and the roles and attitudes of each market player with this regard.

Generally speaking, in the economy the interest rate has several functions:

So, based on the above functions it clearly appears why this topic interests all the actors involved in the financial environment.

With specific regard to microfinance, the main players involved in the industry (Investors, Intermediaries and MFIs) have different sensitivity to the level of interest rate which initially was primarily focused on providing access to financial services, without paying too much attention to the final cost for the borrower.

Microfinance institutions, like any other investor, are risk adverse, therefore they take great care of analysing risks associated with the required rate of return.

Indeed, as risk is a measure of the degree of uncertainty associated with the return on one asset related to an alternative asset, the MFIs are often concentrating too much on cover themselves to any potential risks and they tend to forget the original purpose of their activity: alleviating poverty.

Based on the material provided by Ms. Urroz, and other discussions occurred during these weeks with members of the faculty, it seems that this trend is smoothly changing towards a more client centric approach, but still a lot of work needs to be done.

The course has given us a clear understanding of all the risks associated to the rate of return, in order to be able to effectively calculate the interest rate the MFI should charge to its clients to cover its costs, be sustainable and at the same time provide a valuable instrument to reduce poverty.

The professor, Ms Sahar Tieby, is Executive Director of Sanabel; the Microfinance Network of Arab Countries.

She has over 20 years of extensive experience in designing microfinance services and streamlining the management of institution’s operations.

During the five days course Ms Tieby gave us the elements to analyse the lending process, how microfinance institutions lend money to low-income persons, get repaid, and cover their operational costs.

Indeed, there is a variety of different strategies to overcome the major micro lending challenges depending on the needs of the target client group, on the conditions in the local environment (economic, social, political, and legal), and goals of the program.

As a result, there are no two completely identical approaches to microlending. However, nearly all microlending programs can be classified as belonging to one of a limited number of microlending models.

Indeed, all microlending programs can be divided into two general categories: individual lending programs and group lending programs.

The course compared these two main categories, giving details of differences between solidarity group, village banking, and other microcredit technologies to explore how they work and the circumstances in which they work best, introducing a framework for managing credit risk and examine how different microcredit methodologies apply that framework.

Individual and group methodologies require different structures of operational and financial organisation. It is important for the most appropriate structure to be selected based on organisational goals, profitability objectives, and risk tolerance to face the four main challenges for every MFI: lack of collateral, information asymmetries, costs, volume.

Main differences between the methodologies:

In summary, interest rates on group loans tend to be higher than interest rates on individual loans. Group lending has lower closing costs but higher maintenance costs and higher overall costs than individual lending.

The course has provided a detailed picture of which are the options for MFIs in order to meet clients’ needs in a proper way.

As stressed by both the professors, microfinance represents an effective way to reduce poverty in developing countries, but much additional effort is needed at each level (individual, community, institutional) to further increase the impact of this industry on the cause of poverty alleviation.

Furthermore, nowadays a different phenomenon is coming up.

Indeed, while traditional commercial banks are scaling down to diversify their portfolio and provide financial services to a new client segment, MFIs are scaling up to enlarge their pool, it appears that there is an unserved portion of people, which does not belong to any institution target….the lower middle class.