It is the third year InFiNe.lu is sending members to the Boulder Microfinance Training through its Scholarship Programme. After a call of applications in January 2017 and a rigourous selection process, Alessandra Nibbio, junior consultant at Innpact received the sholarship.

She is now in Turin attending the intensive 3 week programme and giving us her insights of the training.

On week 1, Alessandra Nibbio decided to focused on:

On Week 2, her focus is on:

On Week 3, those topicsare the focus:

As junior consultant at Innpact, supporting one of the major global microfinance funds, I chose to attend for the first week at the Boulder training, courses focusing on financial analysis to strengthen my knowledge of the microfinance institutions and their environment, with the idea once back to Luxembourg, to make a more conscious contribution in my daily work.

Because of that, before starting the training, at some point I was concerned not to get inspired enough and to have pushed too much on the quantitative aspects, instead of having balanced a bit more to take courses on the genuine side of microfinance, which is made by people and their stories of success.

I did not know at that time what was waiting for me….

Indeed, every day starts with a plenary session, which touches every time a different topic to give you a flavour of which are the incredible number of faces this sector can have.

As this year the entire training is putting a strong focus on a brand new topic in the industry, Digital Financial Services, the first main speaker taking part into the roundtable was Ms Leora Klapper, lead economist in the Finance and Private Sector Research Team at the World Bank.

She presented an extraordinary resource, which collects all the information you may be interested in about financial inclusion: the Global Findex.

She showed how, through the collection of numbers and figures, financial inclusion can make incredible progresses and expand, because organizations can have a better pictures on what to focus and to improve.

It seems impossible, especially if you come from Europe, but from this big database it results that nowadays just 62% of the world’s adult population has a bank account and there are still 1.3 billion adults in developing countries which pay their trash, water, and electric bills in cash, as well as school fees.

In this sense, there are still big opportunities to expand financial inclusion and although account ownership represents a first step towards this journey, what really matters is whether people actually use their account and if they have been trained and educated adequately to do so.

So, the conclusion of this debate was that everything should start from education and from MFIs support to clients, in order to make them independent people, able to manage their daily life and their money in an efficient way.

This first session was already enough to make me understanding that, I am in the right place at the right time.

All of these open debates and all the talks I will have every day with several people working on the field, will contribute to the inspirational side I was looking for.

Actually, my current feeling is that here at Boulder there is never a lack of one of the two main components of microfinance: human beings stories and finance.

But let’s go back to finance again for a moment.

The two courses that I mentioned before, taught by Mr Aldo Moauro and Ms Petronella Chigara-Dhitima, are called “Financial and Social Performance of microfinance institutions” and “Financial Analysis for Microfinance Institutions”.

Both courses are aimed at illustrating the methodologies and processes to assess financial and social performance of Microfinance Institutions.

The more interesting part these days was to see the evolution over time from microcredit to microfinance to financial inclusion and how this sector has promptly improved in a relatively short time the analysis of credit and financial risks.

The courses explain how to interpret financial statements and adjust them in order to perform benchmarking analysis and calculate key ratios to measure and evaluate portfolio quality, efficiency, and profitability.

In addition, based on a high participatory approach and group discussion on case studies, you find out at the end of each lesson that you get closer of being able to quantify and gauge the risks inherent in MFIs, and choose strategies to improve performance for sustainability.

Some inspirational and financial readings which come from these courses and that I would strongly recommend you:

This year the Boulder Microfinance Training has recognised Digital Financial Services (DFS), as one of the “hot topic” for the microfinance sector, to the extent that it has been created a specific concentration, offering 8 courses dedicated exclusively to DFS.

On my side, I chose the “Development” concentration, which is specifically designed for professionals especially interested in microfinance as a means to alleviate poverty, increasing financial inclusion with client centricity and empowerment.

However, due to the large interest demonstrated by all the training participants for digital financial inclusion, the Boulder Institute organised a special session, on July 20, to introduce the main aspects of this industry, which I decided to attend to satisfy my desire to learn more.

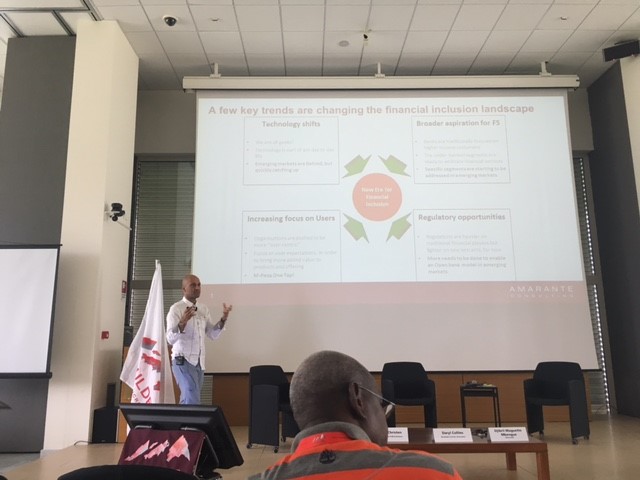

This session led by Mr. Aiaze Mitha – founder of Amarante Consulting and consultant for IFC, specialized in providing advisory to mobile operators, financial institutions and policymakers on their mobile financial services initiatives, was intended to give an overview of the digital finance landscape and present this new way of engaging with customers and delivering meaningful financial services globally.

Mr. Mitha mainly presented a general overview of 2016 results and future trends, but first of all he explained what “Digital Financial Services” stand for.

Digital Financial Services are alternative lending options, which have grown rapidly in developed markets over the last ten years and which are now approaching also developing countries.

These new ways of lending are linked to the emergence of smartphones worldwide, which has provided a new access point to customers through the internet or an app and it could change the digital credit market structure significantly.

Mr. Mitha underlined that we have just entered a new era for financial inclusion, for which technology represents the main enabler.

Indeed, none of what we have seen emerge in the last decade would have been possible without technology.

However, technology on its own is not sufficient as it needs to be strictly related to distribution.

With this regard, Mr. Mitha stressed that to access digital financial services, access to a mobile connection is important, but it is equally important to be able to convert cash to digital money and then back into cash again.

Mobile phones have been important in particular in Africa, in countries such as Kenya, which currently as 37 MFIs equipped for digital finance, but the real turning point has been the emergence of large and well-functioning agent networks.

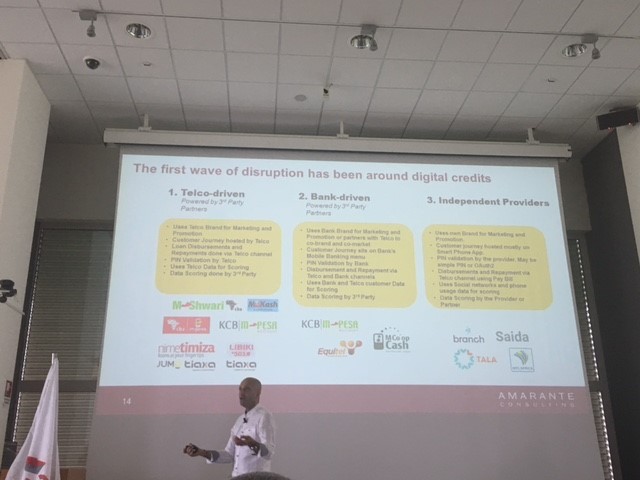

Many partnership have emerged for offering digital credit and are differentiated by who owns what part of the digital credit value chain.

In developing countries, mobile network operators (telco) have a dominant role because they own key assets of the value chain, such as access points, payment accounts and data pools.

They can acquire balance sheets as a commodity through partnerships or lending licenses.

There are currently three different models which allow people to access digital finance:

As a matter of fact, until accounts are more widely available or people are willing to accept the leap into purely digital money, agents will remain indispensable.

With regard to technology, emerging markets are behind, but quickly catching up.

In this process, a crucial role has been played by Regulations, as it appears that they are currently more restrictive on traditional financial players than on new entrants, enabling digital finance to grow rapidly.

Governments are increasingly channelling payments to citizens through digital infrastructure and, in some markets, citizens are able to pay governments too.

Given the large volumes of money drives through the system, this is having an important impact on the viability of digital finance operations.

The main impact that global financial policy can have on emerging markets is particularly related to the effect of de-risking these markets.

As the growth of digital credit is likely to continue, there is the emergence of collaborative approaches between the commercial sector and the public sector to help broaden the digital ecosystem.

The result of the discussion led by Mr. Mitha is that, although digital credit is not intended to replace other formal lending but to complement it, it may shift the current supply-side structure towards more fintech-led models because it provides a low-cost channel to the customer and their data.

The microfinance industry may well be evolving into a more digital operating model, but existing digital credit services address a different need.

Indeed, the primary purpose of digital credit is to provide short-term liquidity to cash-strapped vulnerable categories, while microfinance and bank loans typically provide longer-term investment capital or other long-term assets.

Expectations for the future is that the inclusive digital ecosystems will continue providing unprecedented opportunities to generate growth and development, leveraging both financial and non-financial services.

Some interesting readings which come from this speech and that I would strongly recommend you to go deeper in the discussion: