As part of InFiNe.lu scholarship programme, InFiNe.lu offered one scholarship to Yves Ferreira, senior investment officer at the EIB, to attend the 2018 Boulder Microfinance Training this summer.

Since this year, the Boulder Microfinance training lasts 2 weeks (compare to 3 the previous years). Here is Yves Ferreira’s insight of the first week of the training organised in Turin from July 23rd to August 3rd. His second week can be read here.

One week before the start of the course, I joined the 2018 Boulder MFT English Program group on WhatsApp. Through the tone of the messages exchanged I could already feel the excitement and positive energy towards this event that is bringing together, on the banks of the River Pô, 235 participants from 61 countries (Latin America has its dedicated gathering on the continent) with some coming as far as Timor Leste or Samoa.

Once on the spot, I was not disappointed as I started meeting people sharing the same passion and talking about their area of activity with so much fervour.

In addition, by having decided to join the English Course I definitely opened the door, in particular during the elective courses, to very enriching exchanges of experience with colleagues from markets to which I have not been exposed at all, Eastern Europe, Middle East and South Asia. Their insights are unique and what an occasion for me to put my Caribbean and African experiences from a different perspective, to challenge my views and ideas on so many subjects.

But this is not the main choice, I had to make to build-up my two-week immersion curriculum.

First of all, I had to choose among the four “concentrations” :

Working for the EIB, a funder of the microfinance sector, the choice was easy towards the third one.

But then selecting four “elective” courses among, every time, three options was a dilemma as you feel like being in more than one place at a time.

At the end, having in mind the imperative need to better understand the realities and challenges our potential and existing borrowers are confronted so I decided to opt for the following courses:

An opportunity for me to go back to the basics and ascertain if, as certain say, group lending is on the decline and individual lending, thanks to digitalisation, is really the only way forward. Maybe reality is not exactly black or white and probably there are different shades of grey to use depending on the local environment and targeted market segment.

I have always been convinced of the fact that having a development impact means reducing vulnerability and breaking the vicious cycle of poverty. Thus, I am eager to learn which financial services can really help customers from the bottom of the pyramid manage the numerous risk they have to withstand to and how, in the era of inclusive finance, MFIs should combine and deploy them.

Digital Finance is fundamentally changing the nature of financial services provisions. That being said, I am mostly interested in knowing what new architecture will emerge and which role Financial Service Providers can still play in it. Can they also contribute to the development of these ecosystems or are they condemned to be irreversibly side-lined by Fintechs?

Digitalisation again, but this time as an opportunity to better cater for the needs of MSMEs and also be more efficient in assessing and managing the specific risk of this segment of the market. I am curious to know about successful alternative business models, if any.

Last but not least this curriculum is complemented by the daily morning attendance by all the participants of the

Boulder Master Class.

This very important component aims at better understanding financial inclusion trends and the strategic implications of regulatory and funding decisions on the industry.

From the ones I have attended so far, there are a certain number of takeaways that are in my view worth sharing.

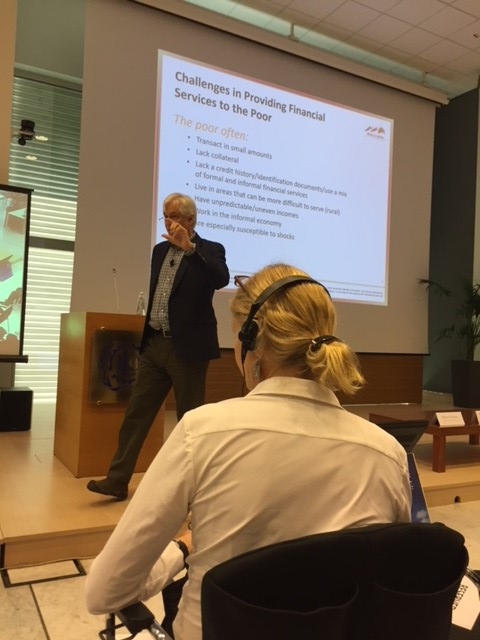

On our first day Robert Christen, President and Founder of the Boulder Microfinance Institute talking about the challenges in providing financial services to the poor did not hesitate to shake the coconut tree and share with us some lessons learned over his 40-year journey. From development finance to financial inclusion passing through microcredit and microfinance providing financial services to the poor has always been synonymous of high transactions costs and asymmetry of information. Group lending in rural areas partly overcame these twin challenges. Microcredit to the informal economy in urban areas was able to charge high interest rates and cover its costs. Microfinance and its search for scale created sustainable platforms (large and profitable MFIS), that provided financial services to a larger number of customers. But then came the 2010-2011 confidence crisis. Some studies concluded there was no link between microcredit and exit from poverty. On the contrary, as in the case of India, it had been synonymous with over-indebtedness and social despair. Compartamos’ IPO was the sign that Microfinance had lost its soul.

In its new search for a soul, the industry has decided to put clients at the center and look for usefulness. Its new aim is to have an impact on people’s lives and further reach the underserved. However, to be able to talk about real financial inclusion it still has to depart from product standardisation and embrace segmentation. It has to crack the demand puzzle.

And if at the end, Microfinance was not about poverty alleviation but simply a way of helping poor people organise their cash flows….

I concluded my first article with reference to segmentation and client centricity as the new frontiers for an industry focused, at the least at the level of intentions, on financial inclusion.

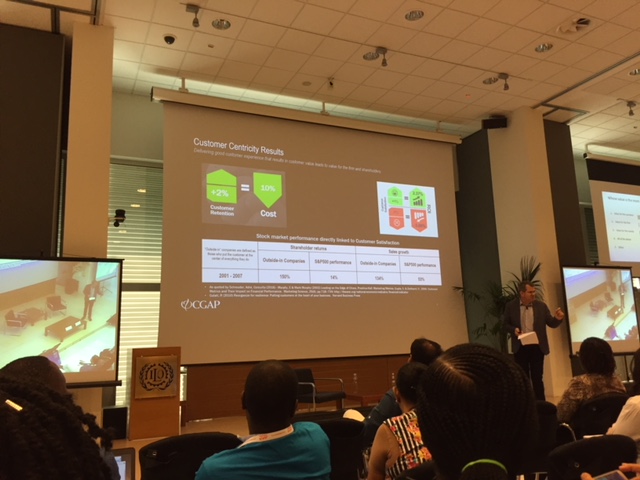

Again, in the context of a Boulder Master Class, Gerhard Coetzee from CGAP, presented to the audience, in a very interactive way, his case for client centricity.

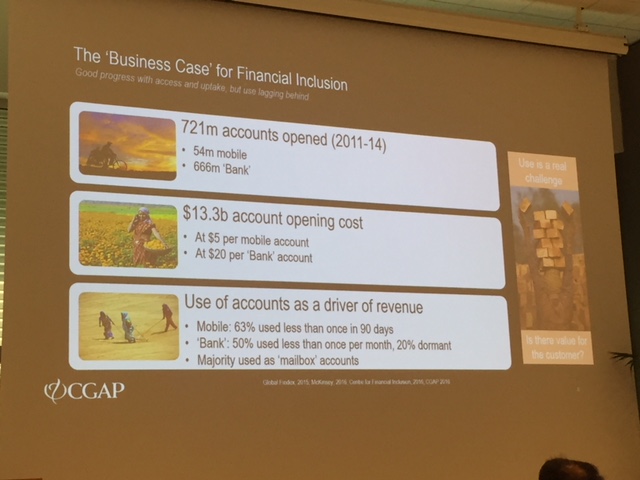

Using as a starting point the figures of the Global Findex Database, and in particular, the ones relating to accounts opening, he stressed on the fact that yes there has been good progress towards access and uptake but the use of accounts, also a driver of revenue, is lagging behind.

And this mainly for the following reasons:

Thus, there is definitely a need to much better understand their expectations and develop the adequate solutions leaving behind the one-size fits all philosophy.

Wishing to take the pulse from the audience (composed of a large number of industry practitioners representing a large variety of jurisdictions) on the subject, Gerhard organised, inter alia, a life survey around the following question:

Most people voted for the second one, revealing that indeed in most markets competition, including sometimes from MNOs (Mobile Network Operators) and Fintechs, is fierce.

In fact, only one or the combination of the four elements above should be the driver for the adoption of a customer-centric business model. Still, such a move has to be considered as a journey for the institution. The latter has to be conscious that it will not happen overnight as it implies shifts in Strategy, Culture, and Structure.

A key pillar in this transformation is customer experience and the fact that the new value proposition will give him a sense of empowerment as his needs will have been really taken into consideration.

But delivering good customer experience also leads to value creation for the firm and its shareholders as illustrated by the examples of customer-centric entities such as Card Pioneer, a micro-insurer in the Philippines, and Digicel Mobile Money in Haiti, two case studies that can be found on the amazing guide developed by CGAP (see link below) that puts together a certain number of toolkits to help financial service providers embrace customer centricity in a comprehensive and incremental way.

Another important concept in Gerhard’s presentation is the fact that Customer Centricity is a business model that operates in an ecosystem of customers, of course, but also of employees, suppliers (including partners), shareholders, competitors and the communities an organisation serves. Thus, according to James F. Moore, who pioneered the concept, only institutions be able to develop mutually beneficial relationships with the other components of the ecosystem will survive. However, one can question the limits of the idea of symbiotic relationships with competitors in the microfinance sector when you see competition meaning poaching of customers, employees or the copying and pasting of products. But I guess, you can take comfort from some wise words pronounced by Robert Chirsten: ” It is easy to copy the form but not the essence”.

So, an institution able to preserve the “essence” and to keep its business model authentically and lastingly customer-centric will always dispose of an edge towards competition.

Another transformation in the making is of course digitalisation, so even briefly I would like to make reference to another outstanding Master Class we had during this first week: Digital Strategy by Ignacio Mas from the Digital Frontier Institute and Aiaze Mitha, an independent Consultant.

Empowerment was again a notion the speakers referred to. Indeed, Digitalisation should mean empowerment shifts for the customer via, in particular, a sense of intimacy and convenience but also for staff within the organisation through a sense of responsibility and control. Indeed digitalisation, when successful, can be synonymous of employees being more autonomous, knowledgeable, and productive in the execution of their day-to-day responsibilities and most importantly, for those dealing directly with customers, being able to respond quickly to their enquiries or demands.

Empowerment was again a notion the speakers referred to. Indeed, Digitalisation should mean empowerment shifts for the customer via, in particular, a sense of intimacy and convenience but also for staff within the organisation through a sense of responsibility and control. Indeed digitalisation, when successful, can be synonymous of employees being more autonomous, knowledgeable, and productive in the execution of their day-to-day responsibilities and most importantly, for those dealing directly with customers, being able to respond quickly to their enquiries or demands.

Making it simple: Employees moral increases and client satisfaction and experience improves.

Isn’t it worth trying?

Useful references:

https://globalfindex.worldbank.org/

https://customersguide.cgap.org/

http://www.cgap.org/publications/customer-centricity-financial-inclusion

http://www.ranjaygulati.com/reorganize-book

(Author: Yves Ferreira)