This blog is relating the experience of Sachin Vankalas, InFiNe.lu’s scholar attending the Harvard Kennedy School “Rethinking Financial Inclusion: Smart Design for Policy and Practice” programme, April 17-22, 2016.

Harvard Kennedy School of Government conducts an executive education program in ‘ Rethinking Financial Inclusion – smart design and policy’. In the third edition of this executive program 41 leaders active in financial inclusion space of 24 countries are attending the course in Harvard from 18-22 April 2016. The participants represent central banks, regulators, Microfinance practitioners, International Financial Institutions and other industry stakeholders of Inclusive Finance industry.

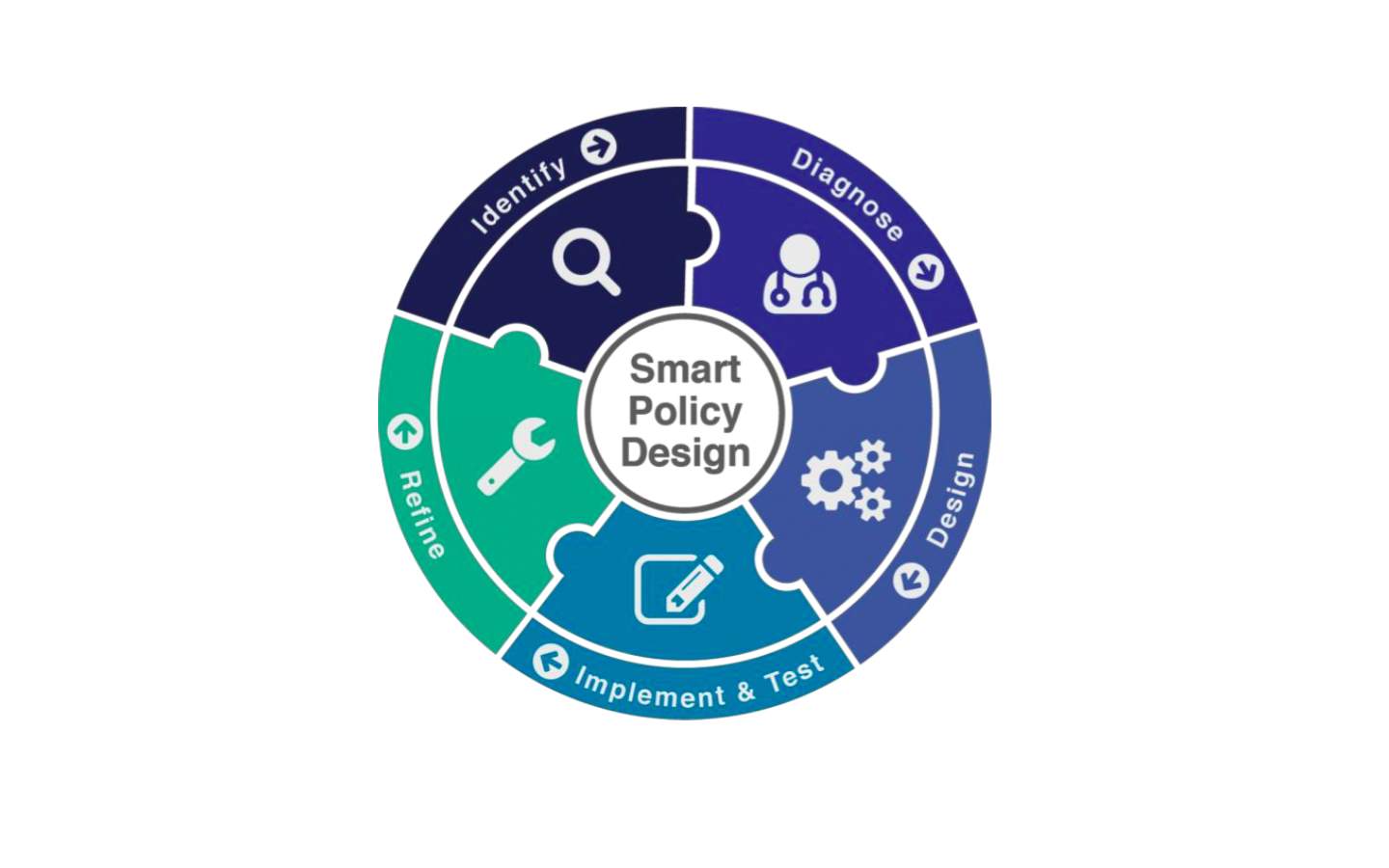

The progam has united leaders in the space around data-driven and evidence-informed design of policies and programs to increase financial inclusion. This week in a series of blog posts, we’ll be diving into some RFI sessions through the lens of Smart policy Design the framework used by Evidence for Policy Design ( E-POD- a unit at Harvard) faculty to teach a problem-driven, collaborative approach to designing, testing, and refining solutions.

Dr Rohini Pande co-director of the program opened the session by introducing concept of Financial Inclusion:

Drawing the ‘unbanked’ population into the formal financial systems so that they have the opportunity to access financial services ranging from savings, payments, and transfers to credit and insurance.”

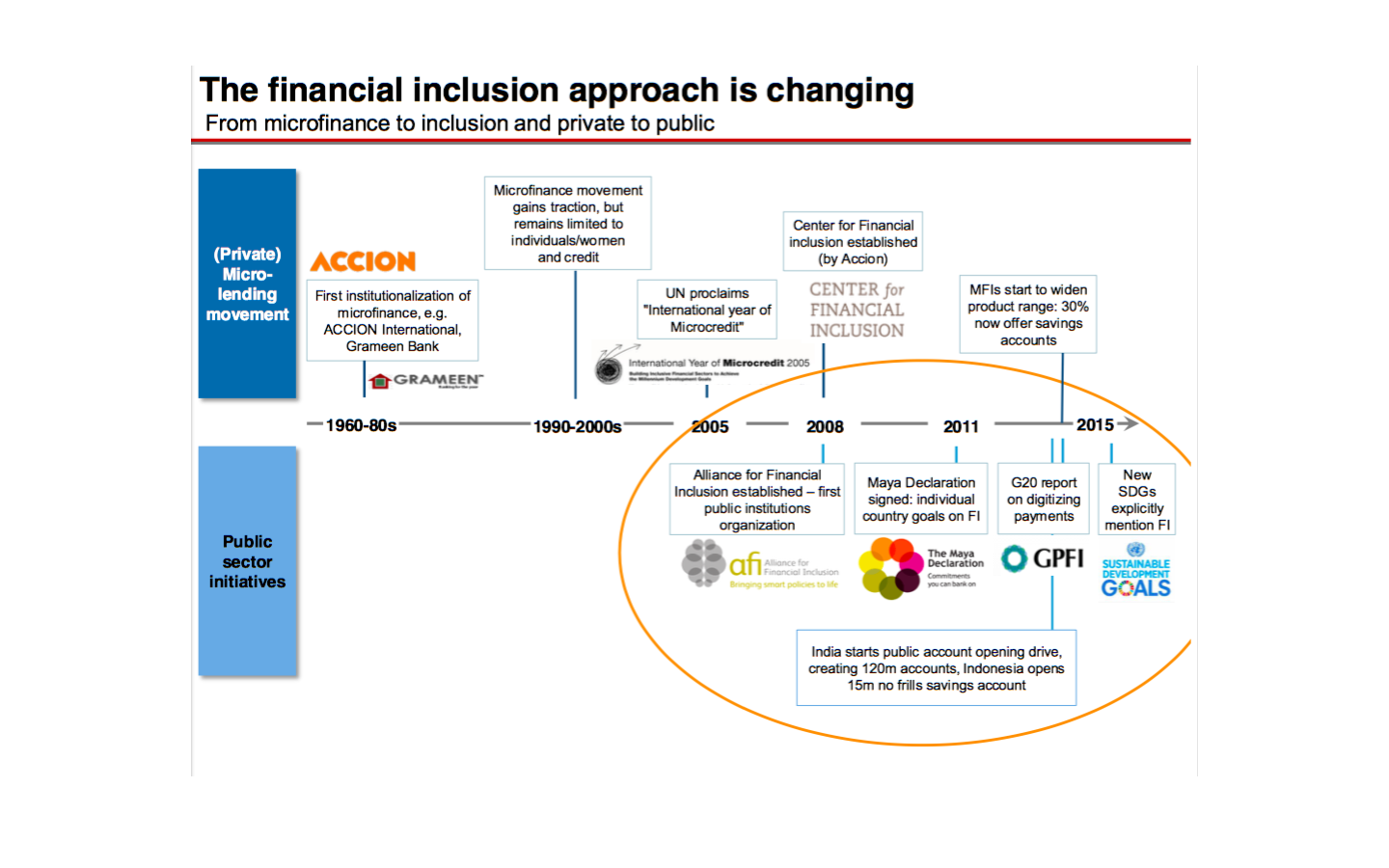

Governments and central banks have been active across the world in building policies for financial inclusion.

Few examples are:

Today’s focus is on successfully identifying a problem with input from multiple stakeholders; we look at a panel discussion EPoD faculty co-director Rohini Pande moderated between Nicole Van Der Tuin (CEO, First Access) and Shivani Siroya (CEO, In on alternative lending models, and a presentation by Rob Wilkinson that walked participants through the negotiating process (one of many tools that will be integral to their work during the course).

In the world of financial services, unbanked users are a great unknown. Beyond the basics of identity verification, not having information about how they’ve behaved in the past makes it next to impossible to know how they’ll behave in future – and has historically reinforced their exclusion from the formal financial system.

The participants looked at great developments happening in the field of big data and mobile banking. What do texting patterns have to do with creditworthiness, you ask? A lot, according to this research, in both the developing and developed worlds. FirstAccess in particular looks at four kinds of data: demographic, geographic, financial, and social. The first two help verify identity and provide context. Financial data provides a pattern of usage: and not only mobile money, as one might expect. Even regular top-up transactions provide incredible value, because they offer a window onto consumption patterns. And research has shown that borrowers with a broader social network are less likely to default, possibly because they have more support in place to help with repayment in the event of an emergency.

Armed with this knowledge, RFI participants broke into guided work groups to begin identifying the policy challenge that we will take on this week. We will be following the Smart Policy Design framework, as will this series of blog posts – we’ll check back in with the groups Wednesday, once the design phase is well underway!

The day started with a case study of on First National Bank of South Africa. FNB introduced a new saving product in 2004 codenamed as ‘the golden opportunity’. In brief, this new account, patterned after successful products in the UK, the Middle East, and Latin America, gave savers a chance to win large cash prizes each month, instead of predictable but unexciting interest. This new savings account, was aimed at bringing new deposits and new customers into the bank, which was locked in a continual struggle with South Africa’s other large banks for market share of retail customers. This product was also aimed at FNB’s commitment to innovation and reach government-mandated goal that the banking sector reach out to the roughly 30 million South Africans who did not use banking services.

Professor Shawn Cole, writer of the above mentioned case study informed the participants about obstacles during the implementation phase of the product and how regulatory intervention forced the bank to stop the saving product which was extremely successful as it brought additional savers.

The day proceeded further with a speech of Sendhil Mullainathan , Harvard Economics Professor specialised on behavioural economics. Mr Mullainathan presented his findings related to ‘Scarcity of resources and its impact on human behaviour’.

As per him, poverty has its root at scarcity, mainly of financial resources. Poor people have more prudence in collecting and handling money as they think about it constantly. For a rich person a five dollar bill represents just a number, whereas a poor person always relate that that five dollar to material things which he could buy. Such as food, clothes, services, etc. It was also mentioned that, the poor often behave in less capable ways, which can further perpetuate poverty.

The professor examined the cognitive function of farmers over the planting cycle. The study found that the same farmer shows diminished cognitive performance before harvest, when poor, as compared with after harvest, when rich. This cannot be explained by differences in time available, nutrition, or work effort. Nor can it be explained with stress: Although farmers do show more stress before harvest, that does not account for diminished cognitive performance. Instead, it appears that poverty itself reduces cognitive capacity. This is because poverty-related concerns consume mental resources, leaving less for other tasks.

Most of the participants found this session extremely thought provoking as it left them in a mixed feeling of clarity on several issues where as confusions on other.

In the afternoon, the group was introduced to importance of big data in financial inclusion space. Big data is not just more the same data but new sources and new methods of data analysis. Cellphone metadata as an example of new source, machine learning as an example of new method. Especially from a regulatory perspective, it is important to remember that now all new users of big data will have solely positive impacts. The participants also looked at persistent questions of users and owners of big data.

Later the participants broke out into guided working group to draft problem statement and define diagnosis for the provided case study.

After identifying the policy issues on fist day sessions and diagnosing the exact problems on second day, the third day of the program was mainly focused on designing solutions for issues identified in Financial Inclusion policy.

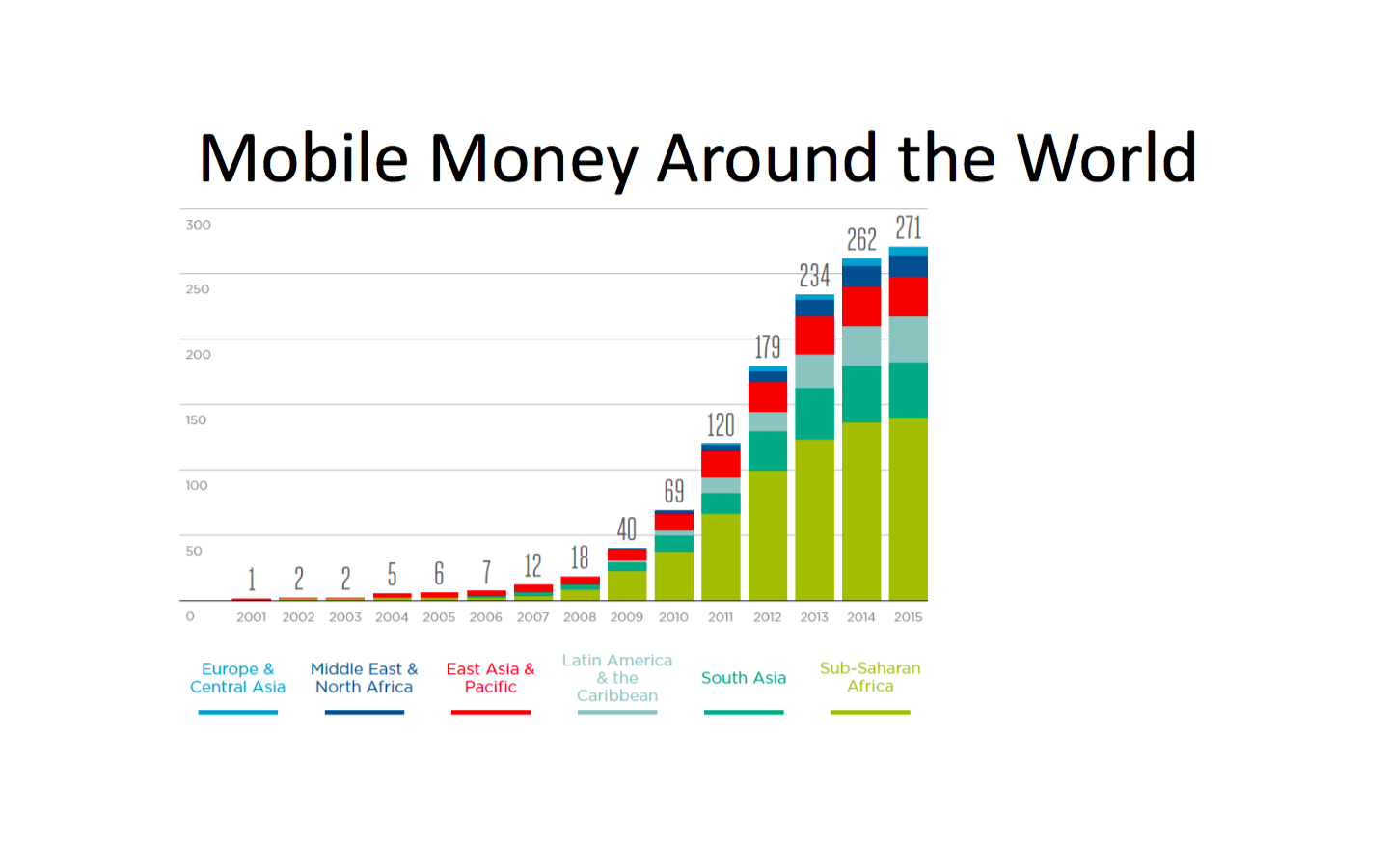

The day started with a case study on M-Pesa -the world’s most successful mobile money transfer service based in a East African country Kenya. Launched in March 2007, M-Pesa (“M” for mobile and “pesa” for “cash” in Swahili, Kenya’s main language) allowed people to use short message service (SMS) messages on mobile phones to send money to relatives living in the countryside or even pay for goods and services, such as groceries or a taxi fare. The service had gained over 1 million users in its first eight months of operations and 2 million users in one year. Safaricom, Kenya’s leading telecom company, operated M-Pesa upon its wireless infrastructure, supported by its innovative agent kiosk infrastructure. The group made an assessment of M-Pesa’s success thus far and what has been key to M-Pesa’s success. We also discussed key challenges facing M-Pesa and what should M-Pesa do to continue to build on its success.

Prof. Shawn Cole from HBS presented a brief summary of developments in mobile payments across the world. It was mentioned that there have been 271 launches of digital financial services around the world in 93 countries but only 25 services have more than one million active accounts. Important to think about why is it so hard?. In the given circumstances regulation highly matters because of network externalities such as payment systems may develop faster in markets with less competition.

After the coffee break, we heard a panel discussion on ‘identifying innovation in financial inclusion’. It was mentioned that the market is moving from focusing on products to focusing on problems. If digitalisation, technology and big data is a way forward for solving the problems of the poor and people in need, we have to also keep in mind the impact evaluation of such projects.

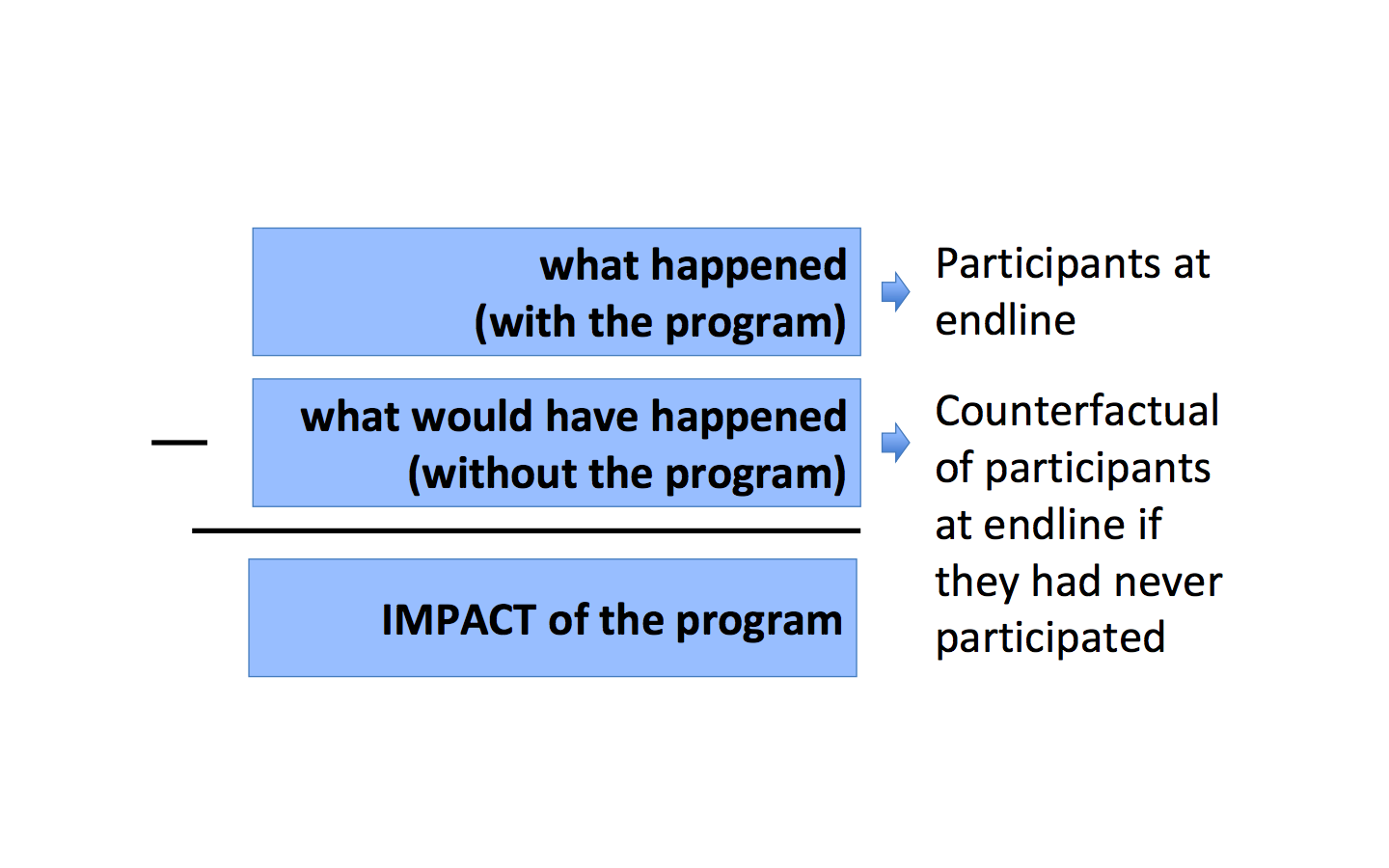

In the afternoon, Asim Khwaja from HKS presented a impact evaluation model for financial inclusion programs. The model had two elements:

The day ended with a group work on designing solution for a given case.

The day started with a case study on BASIX – a well known MFI from India. In the spring of 2004, N.V. Ramana, managing director of KBS Bank in Mahbubnagar, India, was thinking carefully about the organization’s recent experience offering weather insurance to farmers. Weather insurance provides policyholders a cash payout in the event of low rainfall during the summer growing season. KBS Bank was part of the BASIX group, a group of companies providing microcredit and other “livelihood promotion’’ services to the rural population.

The new insurance policy had been marketed in two villages in the summer of 2003. Because of the novelty of the product, BASIX’s deployed its best sales force (customer service agents, or CSAs) to sell the policy. Only 148 farmers had elected to purchase the policy, paying a total of approximately Rs. 74,000 ($1,800) for coverage of 600 acres of land. As BASIX earned only a 15% commission on policy sales, the revenue was negligible, especially when compared to staff time spent developing and familiarising farmers with the new product.

However, the decision of whether to continue to offer the new product would depend not only on this pilot but on the long-run potential of the product to advance BASIX’s mission and its clients’ interests.

The group with the help Prof Shawn Cole from Harvard Business School worked on questions such as what fundamental problems Basix’s customer face? how does the proposed rainfall insurance program work? If the Monte Carlo simulation is to be used what does the existing model tell about pricing efficiency of the insurance contract?

It was mentioned that learning from Basix experience, institutions in over 10 countries started offering rainfall insurance around the world.

Next decade may see significant improvements as:

Following coffee break, we had a a panel discussion on ’ testing innovations on digital finance’. Academics as well as practitioners from the field provided significant input on how digitalisation of services is significantly improving service offer and how it may affect on organisational structures.

After the lunch break, Prof Khwaja presented Impact Evaluation module.

It was mentioned that in any Impact Investing program, the counterfactuals play most important role. Therefore, they must be selected very carefully.The impact evaluation must include information on:

Afterwords, the participants spread out in working groups for finalising their presentation on given topics.

The outcomes of breakout sessions were presented by each working group leader. Nine groups each composed of 5 participants developed a detail report on a given topic. The reports were composed on identification of the issue, diagnosis, program design, testing and refine and final solution.