This week’s module was about “building partnerships and a digital financial ecosystem”. Innocent Ephraim, who is a consultant with extensive experience working with Fintech and MNOs, in particular in East Africa, presented the module.

As an introduction to the module, Innocent Ephraim recalled the various opportunities digital finance (and in particular mobile money) could create for an MFI:

Mobile money can be delivered in two main ways: over the counter (with the assistance of an agent) or through a mobile wallet. Mobile wallets are a very powerful tool in the sense that they allow the delivery of many services: money transfers, purchase of airtime, bill payments, online payments, merchant payments, savings, loans, insurance, investment services…

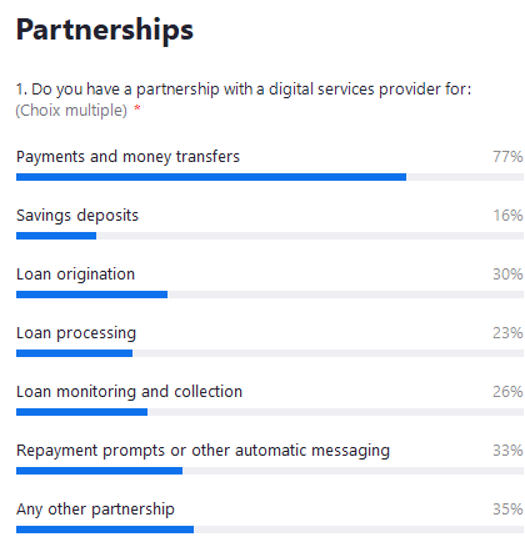

As detailed by Mark Flaming, Aiaze Mitha, Michel Hanouch, Peter Zetterli and Greta Bull in a paper2, “mobile financial services implementations are structurally complex, typically requiring expertise in banking, telecommunications, technology, marketing and distribution. Rarely will one company have the core competence to perform all of these functions efficiently”. For MFIs, building their own mobile money service is usually very costly and complex. Most of them do not have the technical and financial capacities to do so and therefore need to collaborate with MNOs or payment providers to access their existing mobile money solutions.

The introduction of other innovative technologies or products also often require building partnerships with new types of institutions, such as Fintech.

For all these reasons, some MFIs are gradually moving towards what is called a “platform model”, with:

To summarise this approach, and as outlined in another paper3 “the MFIs that will survive the next 10 years will not know every client personally. They will acquire customers through a variety of channels and service them through other channels. The institutions that are able to build the right bundles of partnerships, products, and channels will thrive—and will help their clients to do the same.”

Success factors in implementing partnerships

As detailed by Mark Flaming, Aiaze Mitha, Michel Hanouch, Peter Zetterli and Greta Bull in their paper4, in order to be successful, partnerships for the delivery of mobile financial services “must enable the [different] partners to generate value for their respective companies”. Part of that value “will come from the product itself” and additional value will come from “the partners’ core businesses”. For example, “banks may benefit from deposit mobilisation, cost savings, and product line growth; mobile network operators (MNOs) may benefit from an increase in airtime sales, reduced distribution costs and client retention; and payment service providers (PSPs) and agent network managers (ANMs) may derive benefits from new customers in their networks and growth in transactional volumes”.

[1] Beyond single source solutions, Innocent Ephraim, FSDT, November 24, 2017

[2] Partnerships in Mobile Financial Services: Factors for Success, Mark Flaming, Aiaze Mitha, Michel Hanouch,

Peter Zetterli, Greta Bull, August 2013

[3] A Tale of Two Sisters, Microfinance Institutions and PAYGo Solar, Daniel Waldron, Alexander Sotiriou, and Jacob Winiecki, November 2019

[4] Partnerships in Mobile Financial Services: Factors for Success, Mark Flaming, Aiaze Mitha, Michel Hanouch,

Peter Zetterli, Greta Bull, August 2013